Navigating Fertiliser Risk over Reacting to Headlines

Dr Dannielle Robb

Apr, 21 2026Fertiliser continues to sit at the heart of arable profitability discussions. It remains one of the largest controllable costs on farm, yet it is also one of the most unpredictable. The focus recent is not on trying to forecast fertiliser prices, but on understanding how growers can make better decisions when volatility is no longer temporary, but structural.

The core message is clear: the greatest risk today is often not the price of fertiliser itself, but risky decision‑making driven by uncertainty, hindsight and headline reactions.

Fertiliser prices are volatile, but the real risk lies elsewhere

The past few seasons have shown just how exposed fertiliser markets are to global disruption. Geopolitical conflict, particularly in Ukraine and the Middle East, alongside ongoing instability in energy markets, has created sharp price swings that feel uncomfortable and difficult to navigate.

However, focusing solely on price obscures the bigger problem. Businesses tend to respond emotionally to volatility, often reacting to the wrong signals at the wrong time. This can lead to missed opportunities, badly timed purchases, or over‑correction in following seasons.

Understanding where fertiliser risk actually comes from is the first step in managing it more effectively.

Understanding the drivers behind fertiliser markets

- Nitrogen must be viewed as an energy product first, and an agricultural input second. Prices are driven primarily by natural gas values, ammonia production capacity, logistics, and geopolitics. When gas prices rise or supply chains tighten, nitrogen prices follow. Crop values, drilling progress, and farmer sentiment have very little influence.

- Phosphate and potash are better thought of as geopolitical minerals. These markets tend to move more slowly but are highly sensitive to exporting nations, sanctions, and shipping routes. Supply is concentrated, which makes prices vulnerable to sudden step changes when disruption occurs.

- Crucially, current market volatility is not temporary. Structural drivers such as global trade realignment, carbon pricing, environmental constraints on production, and geopolitical tension mean that input markets are likely to remain unstable for the foreseeable future.

The question is no longer when prices will return to normal, but how farm businesses can operate profitably in a permanently volatile input environment.

The current fertiliser landscape

As of spring 2026, fertiliser markets remain tight and nervous.

Global urea prices are being propped up by disruption risk around the Strait of Hormuz, through which around 30 percent of global urea shipments pass. With periods of production offline and strong buying interest from India, prices remain elevated.

In the UK, ammonium nitrate prices are firm, supported by constrained European production and high raw material costs. NS compounds are increasingly difficult to source, with little new stock expected. Liquid nitrogen remains available and can still be cost‑effective for applications such as earwash, particularly where milling premiums are modest.

Phosphate fertilisers such as DAP and TSP are available but expensive, limiting flexibility for maize and spring cropping decisions. MOP has so far avoided the sharp price rises seen elsewhere, although it is not immune to future increases.

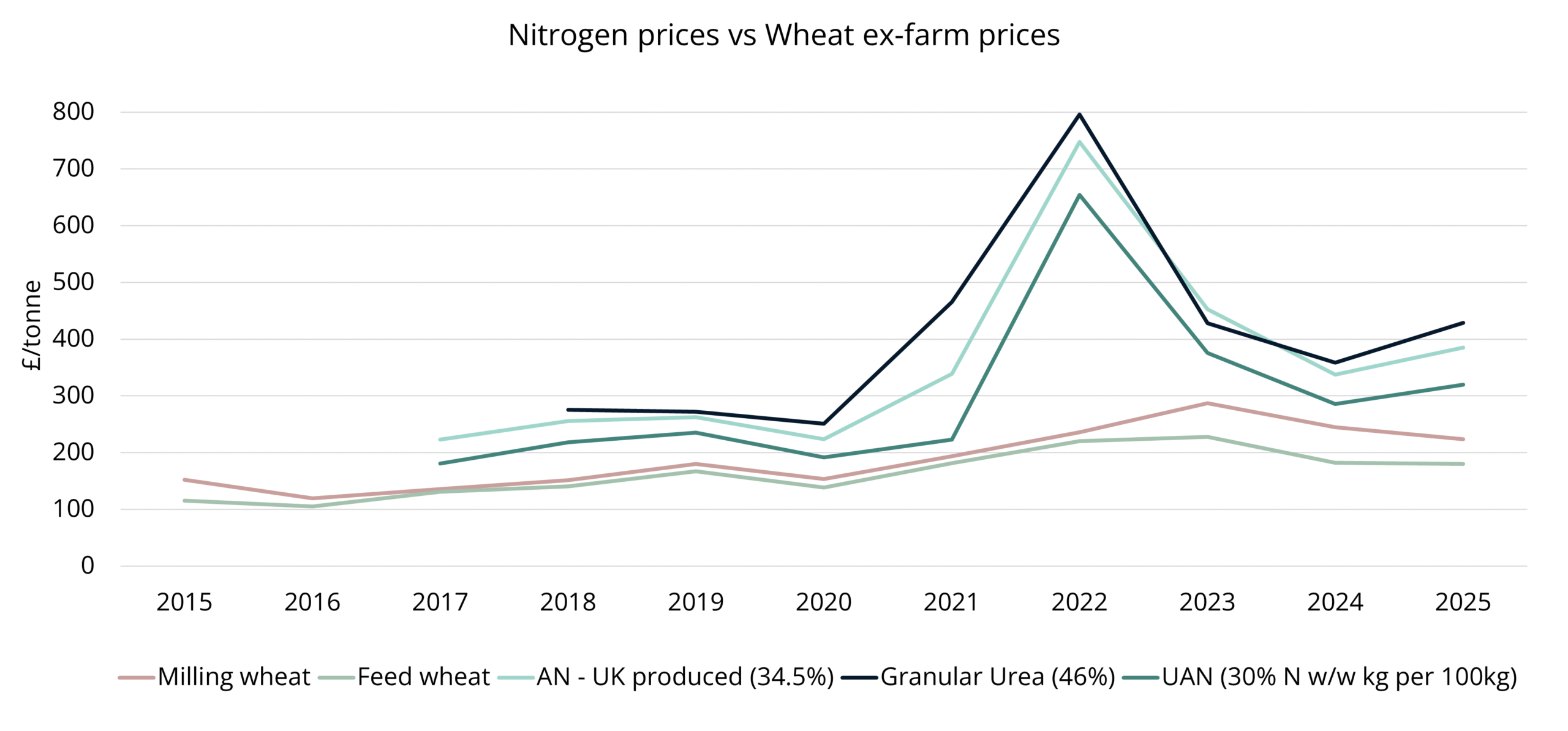

Putting fertiliser prices into a UK context

Viewed in isolation, fertiliser prices look alarming. However, when set alongside UK wheat values, a more nuanced picture emerges.

Crop prices have also moved to a higher average level than pre‑2020, helping to offset some of the increased input cost pressure. Affordability is strained, but not unprecedented.

Looking back over the past decade reinforces this point. The extreme spike in fertiliser prices during 2022 was exceptional, but prices never fully returned to earlier norms. Similarly, wheat prices now sit on a higher plane than during the 2010s.

The key shift is that both inputs and outputs are now more volatile, increasing the consequences of poor timing and emotionally driven decisions.

Figure 1. Nitrogen prices vs Wheat ex-farm prices. Source: AHDB.

An exit strategy for a volatile world

Rather than chasing the lowest possible fertiliser price in hindsight, develop strategies that reduce exposure and protect margin.

Key principles include:

- Accepting volatility as permanent, not temporary

- Stopping attempts to time the market

- Buying fertiliser in tranches rather than committing to total requirements in one go

- Linking fertiliser purchases to crop margin and, where appropriate, forward grain pricing

- Investing in nutrient efficiency to reduce exposure over time

- Protecting certainty through written strategies, price triggers, and pre‑agreed decisions rather than emotion.

In volatile markets, the goal is not perfection. It is avoiding catastrophic outcomes and preserving business resilience.

From market strategy to field decisions

Understanding fertiliser markets is only half the picture. The real challenge is translating that volatility into sensible nitrogen decisions in the field, particularly in a dry spring where crop response is uncertain.

We explore this practical reality in a follow‑on members article focused on nitrogen decision‑making under dry, variable conditions, including where flexibility exists and how to avoid irreversible decisions too early in the season. You can read this article here, or re-watch our Monthly Agronomy Club here where we discussed these topics in even more detail.