Global Weather, Grain Markets & Nitrogen

Ceres Research

Mar, 20 2026While much of the agronomic conversations are focused on upcoming fungicide and spray programmes, the market outlook for wheat and fertiliser is just as important for shaping spring decisions. Here’s what’s driving the market and what it means for farm businesses in Spring 2026.

US Winter Wheat Under Significant Heat Stress

One of the biggest market movers right now comes from the US Plains, where winter wheat crops are battling heat and drought stress.

This includes:

- Severely low soil moisture, particularly in Kansas – one of the largest US wheat‑producing states.

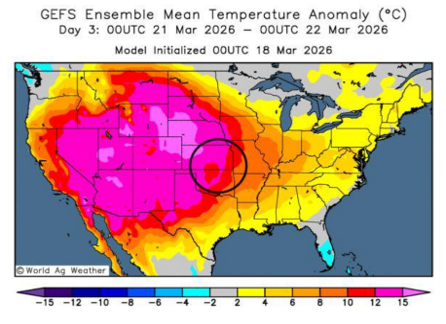

- A forecast showing temperatures up to 15°C above normal, with some areas expected to hit 30°C next week.

- Worsening crop condition scores across several major wheat states.

Figure 1. Example heat map of the US showing temperature anomalies between 21st and 22nd March 2026.

Why this matters:

Tighter US supply expectations tend to support global prices, especially for milling wheat. With US crops under pressure so early in the season, the market is on alert for further deterioration.

UK Wheat Imports Slow – Tightening Domestic Balance

Closer to home, the UK wheat balance sheet is showing signs of tightening:

- Imports from July–January are down 443kt compared with last season.

- Total wheat imports currently sit at 1.5 million tonnes.

A slower pace of arrivals generally supports domestic basis, particularly in regions dependent on imported milling wheat. If the trend continues into spring, UK buyers may need to stay more active in the market to secure coverage.

Fertiliser Markets: Post‑War Highs and Big Supply Disruptions

Fertiliser markets remain volatile, with several geopolitical and supply‑chain issues adding upward pressure:

- Iran has destroyed 16 commercial vessels in the Strait of Hormuz in the first two weeks of the conflict, disrupting critical nitrogen transport routes.

- Both energy and fertiliser markets are now trading at post‑war highs.

- High nitrogen prices are already influencing planting choices:

- US growers shifting towards soya

- EU growers leaning to sunflowers or lower‑N alternatives

This shift reduces demand for N‑heavy crops and indirectly supports global grain prices.

A Rare Inverse in the Fertiliser Market

One notable trend is the extremely strong market inverse:

- Spot prices are significantly higher than forward values

- May–August forward nitrogen is currently ~30% cheaper than today’s spot

This suggests the market is pricing in a short‑term supply squeeze, driven by transport disruption rather than long‑term scarcity.

Practical takeaway:

Growers may benefit from flexible purchasing strategies this spring, particularly if cashflow is under pressure. But any delayed buying comes with the risk of short-term availability issues.

Regulation to Watch: UK CBAM Nitrogen Tax

The UK is considering its own version of CBAM from January 2027, which could further complicate the regulatory landscape and pricing structures. Still, the CBAM coming into effect in the EU from 2026 will have implications on the UK ahead of 2027. Early modelling suggests an uplift of £50–£70/t. This could incentivise greater use of urea, which is more nutrient-dense and may perform better under CBAM rules. You can read more about this new potential carbon cost here.

What Should Farmers Be Thinking About Now?

Given the current climate, wheat and fertiliser markets will remain sensitive to:

- US crop ratings over the next 4–6 weeks

- Ongoing logistics disruption in the Middle East

- UK import pace and domestic demand trends

- Spring nitrogen buying behaviour

- Regulatory pressure on fertiliser types and timings

For growers, this means staying flexible and well‑informed. Both grain and nitrogen markets look set for another turbulent season, but understanding the forces behind them can help keep decision‑making grounded.